Scott Liddicoat

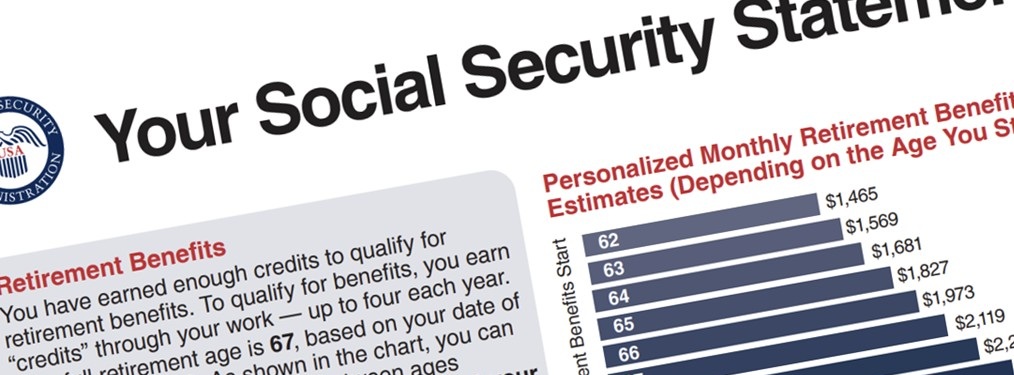

Retirement’s looming, so I’ve been inspecting my Social Security “statement” online. It provides a table of my yearly taxable income. Along with it is a list of what they’ll pay me each month depending on the age I start to draw “benefits.”

There’s no account balance I can claim I own. No statement of earnings on my “contributions.” Worse yet, politicians say my benefits may be decreased with changes in legislation or population demographics. These things would never affect an account I actually owned.

Too bad. I would have turned this into a real retirement asset if I could have invested my money, even in just an ordinary money market account. Or in bank CDs.

Heck, I’d probably have done better with my Social Security in a simple savings account.

Of course, all of this is because I don’t really have a Social Security account. My “contributions” to Social Security are immediately paid out to current retirees and other beneficiaries.

What’s left goes to pay daily government bills. This has gone on my entire adult life. The money I’ve paid in isn’t invested on my behalf. Nor is it held in an account under my name. The money I’ve paid in is gone.

I’ll have to depend on young workers paying their “contributions” to fund my Social Security “benefits.

This Ponzi scheme would land private retirement plan administrators in prison. They’d be branded “greedy corporate executives.”

So, what should we say about the elected officials misappropriating our Social Security today? Everyone now, repeat after me: “greedy federal politicians.”

For decades I’ve been paying the “benefits” for those receiving Social Security. I sure hope younger workers, “contributing” these days aren’t very alert. I don’t want them wondering why they’re being forced to pay for my “benefits” out of what they pay into Social Security today.

[Not me…stock photo.]

No Artificial Intelligence was used in the writing of this piece.